Ripple Completes $50 Million MoneyGram Investment, Supporting XRP Use for Global Payments

November 25, 2019

New GMiner 1.80 With Support for Cortex and Additional Ethash Coins

November 26, 2019

When it comes to the federal reserve, there’s levels to understand. You’ve got the federal reserve, located in Washington, D.C, home to the chairman of the Fed and the members of the Board of Governors. But then you’ve also got several regional branches of the federal reserve — twelve, to be exact — that play their own roles within the national banking infrastructure.

If you’re unclear on the purpose of these regional federal reserve banks, what they do, how they function, and why they’re important (or not), we’ve got you covered. We answered some basic questions (you didn’t ask them, but we answered anyway) about the twelve federal reserve banks, and we’re hoping that those answers will clear up any uncertainty you may have.

What’s the history of federal reserve banks?

When the Wilson administration proposed establishing a national bank circa 1913, there was clear upside to the proposal. A unified national banking system would, in theory, help stabilize the national economy and serve as a better framework for regulatory oversight. The central bank would also provide unprecedented liquidity between member banks and standardize reserve requirements, a key lever for manipulating the money supply.

Source: Federal Reserve

But there was also opposition, with one concern being that a single central bank located in Washington, D.C would not adequately serve or represent the varying attitudes and demographics that existed, and still exist, across America.

And so the 1913 Federal Reserve Act would ultimately include a charter for twelve regional banks to serve as operating arms of the D.C.-based federal reserve. They would prove to be critical in maintaining the health of not only the domestic and global economies, but also the existence and integrity of the smaller financial institutions that makeup the American banking network.

What is a federal reserve bank?

Federal reserve banks are extensions of the Fed, and function according to policy set by the twelve-member Federal Open Market Committee (FOMC). The FOMC dictates the policies that we collectively dub “monetary policy”, a term that remains murky at best to most Americans. In fact, 41.2% of respondents in our recent study How Well Do Americans Understand Money? 2019 answered incorrectly when asked “who decides if and when more US dollars should be created?”.

The correct answer: the Fed, specifically the FOMC.

You should know that the FOMC is comprised a seven-member Board of Governors and also five heads of the twelve regional federal reserve banks. So, in a way, the regional federal reserve banks (through their presidents) do have an impact on monetary policy, but those banks mostly follow orders — how much money to keep in reserves, how much can be lent out, what interest rates to charge, etc.

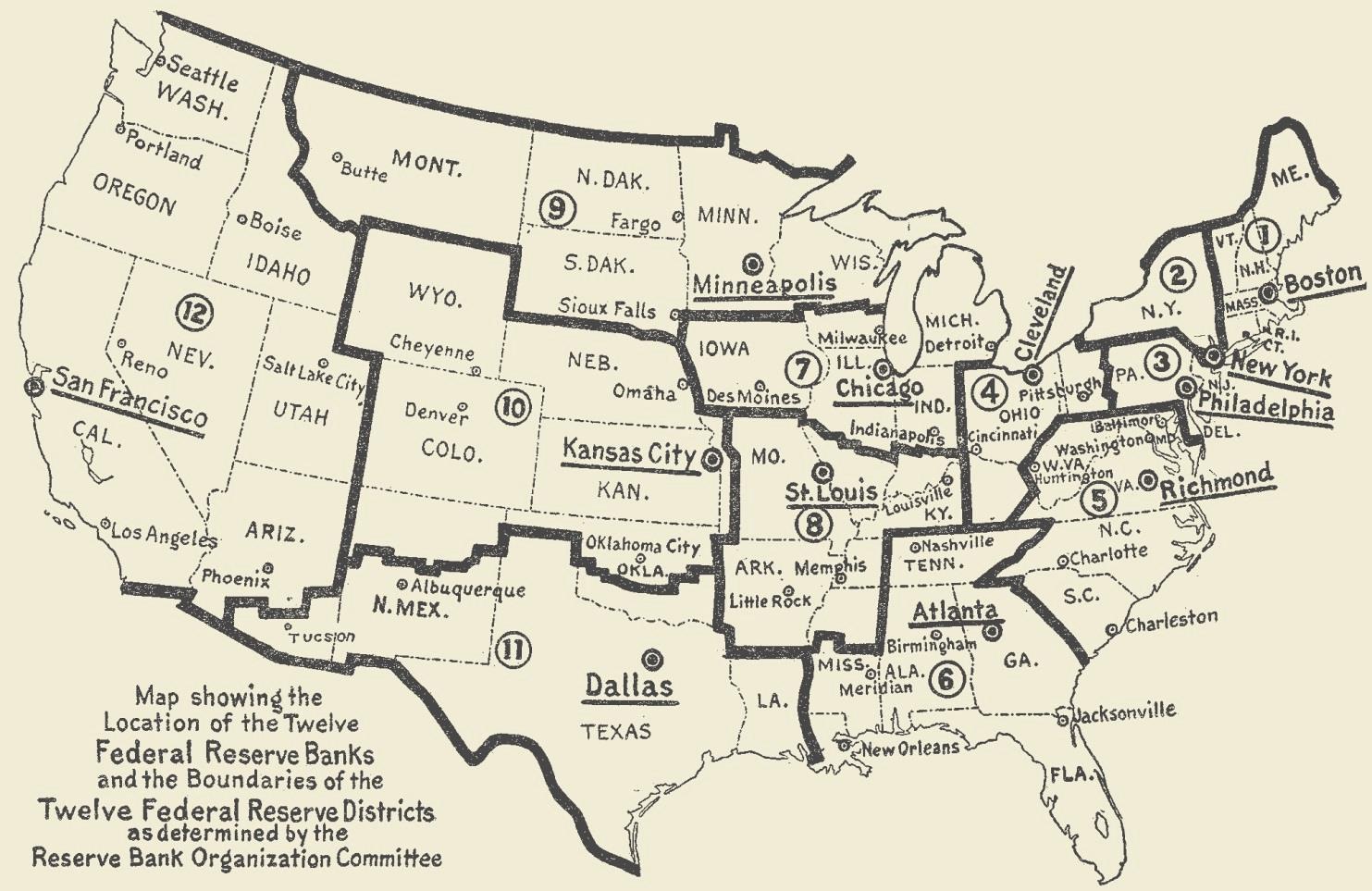

How many federal reserve banks are there, and where are they located?

Excluding the real-deal Fed that resides in Washington, D.C, there are twelve Federal Reserve Districts, with each serviced by a regional federal reserve bank. The districts are skewed towards the east coast, as is reflected by the banks’ locations.

Source: fraser.stlouisfed.org

The cities with a federal reserve bank are (from West to East) San Francisco, Dallas, Kansas City, Minneapolis, St. Louis, Chicago, Atlanta, Cleveland, Richmond, Philadelphia, New York, and Boston.

How do federal reserve banks work?

Regional federal reserve branches serve as depositories for smaller banks. They maintain accounts for smaller financial institutions, and guarantee those deposits for future withdrawal, which is precisely the role those smaller institutions fill on behalf of their customers (us). Regional federal reserve banks also extend loans to financial institutions at a rate set by the FOMC, known as the discount rate.

Federal Reserve Banks As Regulators

Just to clarify: the Federal Reserve System includes the Fed in Washington, D.C., the twelve regional federal reserve banks, and smaller member banks that fall under the purview of those twelve regional banks, according to their geographic location. The twelve regional federal reserve banks serve as a ground-level regulator of the roughly 7,800 member banks that have chosen to join the Federal Reserve System.

Regional federal reserve banks are tasked with ensuring that member banks in their district are complying with Fed-set monetary policy and are not engaging in risky banking practices — cough subprime mortgages cough. While history has proven that oversight from regional federal reserve branches is imperfect, it is something.

As Service Providers for the U.S. Treasury

The regional federal reserve banks act as a sort of checking account for the U.S. Treasury by issuing and redeeming government securities. They also collect unemployment, income, and excise taxes on behalf of Uncle Sam, ultimately handing that money over to the Treasury. Regional federal reserve branches also store collateral on behalf of the federal government for dealings with private institutions and make interest payments on behalf of the U.S. government.

Though the twelve federal reserve branches are technically not for profit, they do increase the money supply and pad their coffers (temporarily) by issuing loans that collect interest. They can also profit from the sale of government securities and through fees on the payment services they provide, but all additional earnings are turned over to the U.S. Treasury each year.

As Financial Service Providers

The twelve regional banks facilitate withdrawals and deposits from the smaller federal reserve member banks in their district. They also extend member banks credit in the form of loans. The regional federal reserve banks clear approximately 18 billion checks each year as a clearinghouse for federal reserve member banks, showing just how critical they are to daily banking operations in the United States.

Who owns federal reserve banks?

Like the main branch of the Fed, the regional federal reserve banks are technically not owned by anybody — not the Fed chairman, not the President, not you or me. They are a part of the independent network that is the federal reserve, which is designed to be above partisan influence or corruption.

Download our Free 13 page Exclusive Report:

The Perceptions of Money & Banking in the US 2019