Tax Office to Contact 350,000 Australians and Remind Them to Report All Crypto Profits

March 12, 2020

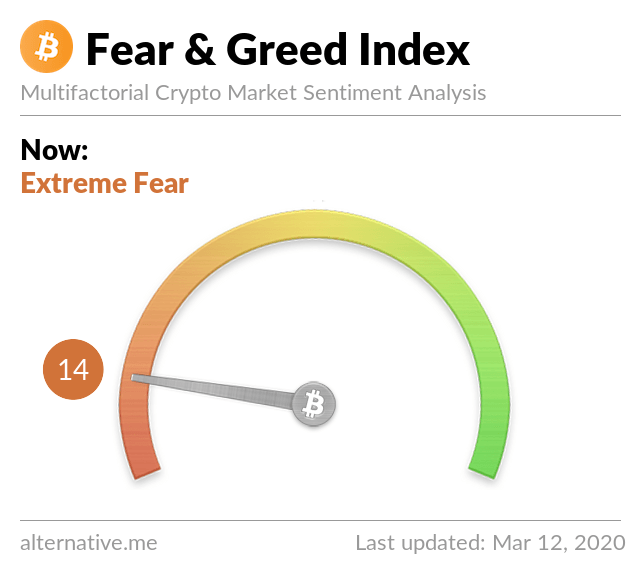

Alternative.me – Crypto Fear and Greed Index

March 12, 2020

The term remittance is not one that you hear every week, let alone every day, and even if you are familiar with the term, you may not understand the nature of the beast that is the remittance industry. In fact, the results of our survey How Well Do Americans Understand Money? could be taken to indicate that widespread unfamiliarity with the remittance industry is a near-certainty. It’s not a knock on anyone — who could be reasonably expected to spend their free time researching the ins and outs of remittance?

With that said, remittance is essentially a fancy way of saying “sending or receiving money from friends or family in another country.” Let’s dive a bit deeper into remittance, including how the remittance industry makes it money and how blockchain-powered alternatives could save money for those who depend on remittance the most: immigrants.

The term ‘remit’ means ‘to send back’, and it is the stem of the word remittance, which generally refers to the act of sending or receiving money from someone in another country. Following this logic, remittances are the funds being sent and received in a given transaction. Though the definition does not suggest this, the term remittance most often applies to international transfers.

Remittance is an essential process, as sending money through the mail is foolhardy while checks can be easily lost in the mail and are simply not practical for most international transfers. There is an entire industry that makes its money from others’ need to send and receive money electronically, often to family members in underdeveloped nations.

As you may suspect, the institutions facilitating remittance payments (with fees charged for each transaction, of course) are the usual suspects — banks and credit unions, primarily, as well as money transfer operators (MTOs) such as Western Union that specialize in cross-border payments.

These institutions take on the cost of verifying the sending and receiving parties’ identities and ensuring that transfers abide by all relevant international regulations, and they take a substantial cut of each transfer in exchange for their services. As of Q3 2019, the average percentage cut taken from each remittance transaction was 6.84%.

The percentage fee that a financial institution can take from any remittance transaction is determined largely by market forces, and these fees can add up to substantial revenue over time. As migration trends increase and sending money across borders becomes increasingly prevalent, newer players in the remittance industry such as TransferWise will continue to emerge to claim their cut.

To put it frankly, the market for remittances is booming. But a closer examination of the groups that are generating the majority of remittances means shining a critical light on the industry as a whole.

According to the World Bank, the total number of remittances sent in 2018 reached a record high of $689 billion, which was a $56 billion increase from 2017. The World Bank also notes that the vast majority of those remittances — $529 billion, to be precise — were sent to low- and middle-income nations.

This statistic hits on what can be perceived as a harsh reality of the remittance industry: immigrants sending money back to their often-impoverished relatives back home are the money-making mechanism for institutions that provide remittance services.

Do these institutions provide an essential service that, overall, provides a net good to the world? Sure. Are all of those institutions ethical in their practices? Surely not.

As an example, consider that immigrants of Sub-Saharan African origin sent a record number of

remittances to their homelands in 2017. Now consider that Sub-Saharan Africa remains the most expensive region in the world to send remittances to, with an average percentage of more than 9 percent taken out of each transaction by financial institutions that process the payments.

Some look at that statistic and assume the best: maybe it is more expensive for remittance processors to process payments in that region of the world, and therefore the higher percentage fee is justified.

Others see such figures and reach another conclusion: that remittance payment processors see prime opportunity to exploit a demographic of immigrants who desperately need to send money home to a largely-impoverished region, and will pay any price to do so.

Regardless of the tint of the lens through which you are inclined to view the remittance industry’s reliance on immigrants, you have to wonder whether there is a more affordable, and in turn ethical, way to send money across borders.

Blockchain is the technology that underpins cryptocurrency, and some see it as a potential market disruptor within the remittance space. The vision: to provide secure remittance transactions at a fraction of the price with unrivaled speed, primarily in service of immigrants who cannot afford to be dishing out even five percent of each payment to financial institutions.

Some early returns suggest that blockchain channels could provide immense improvements in terms of speed of transaction and the cost of sending remittances. According to a BlockData report, blockchain-powered remittance channels settled payments 388 times faster than traditional, non-blockchain channels.

Though it will take time and significant investment to create market-ready remittance channels to compete with the Western Unions of the world, several startups have raised significant funding towards this goal of a robust, blockchain-powered remittance payment network accessible to the average immigrant or anyone else who needs to send money to friends or family in another country.